Buyer Bright Spot: The Housing Inventory is Growing

The past few years have been challenging for homebuyers, especially with higher home prices and mortgage rates. And if you’re trying to buy a home, it’s easy to worry you won’t be able to find something in your budget. The housing inventory has been increasing since 2024.

But here’s what you need to know. The housing inventory has grown a whole lot lately and that’s true for both existing (previously lived-in) and newly built homes. Here’s a look at those two bright spots for buyers right now and why they may make it a bit easier to find the home you’re been looking for.

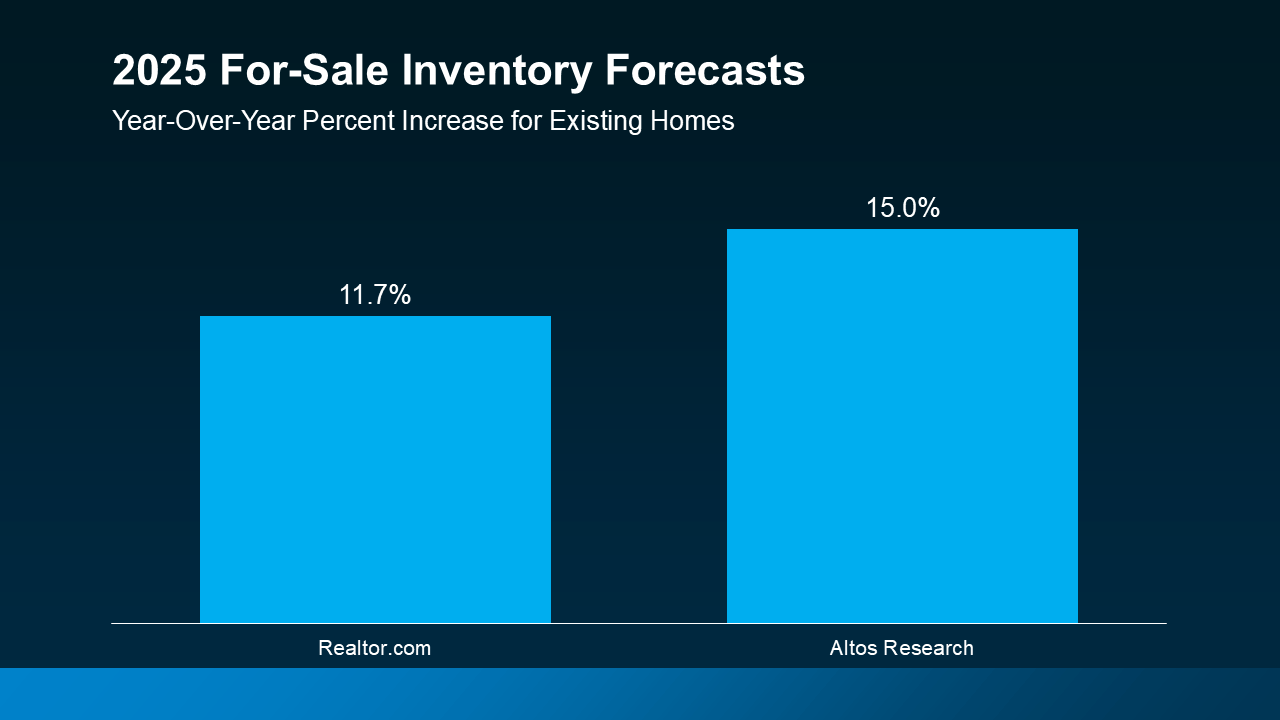

1. There Are 22% More Existing Homes for Sale

Data from Realtor.com says the number of existing homes for sale improved by an impressive 22% in 2024. And experts say your pool of options is expected to get even better this year. Forecasts show inventory is projected to grow another 11-15% by the end of this year (see graph below):

Here’s why this is so good for your search. If you haven’t seen a house with all the features you need, just know that, as the number of homes for sale grows, you’ll have more options to choose from. That means a better chance of finding a home that checks all your boxes. As Ralph McLaughlin, Senior Economist at Realtor.com, says:

Here’s why this is so good for your search. If you haven’t seen a house with all the features you need, just know that, as the number of homes for sale grows, you’ll have more options to choose from. That means a better chance of finding a home that checks all your boxes. As Ralph McLaughlin, Senior Economist at Realtor.com, says:

“It could be a particularly good time to get out into the market . . . you’re going to have more choice. And that’s not something that buyers have really had much over the past several years.”

2. There Are More Newly Built Homes on the Market

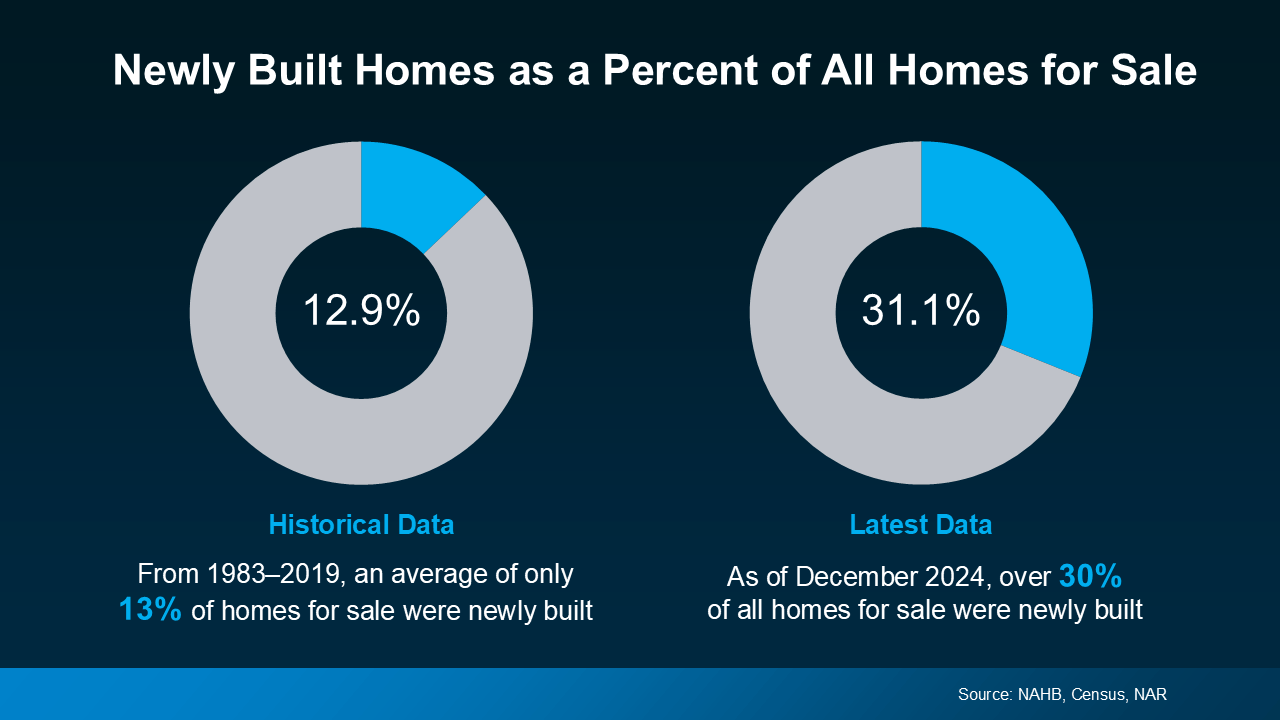

According to data from the Census and the National Association of Realtors (NAR), 31.1%, or roughly 1 in 3, homes on the market right now are newly built homes. That’s more than the norm (see charts below). But don’t worry, that’s not because builders are overdoing it – it’s just that they’re trying to catch up after years of underbuilding.

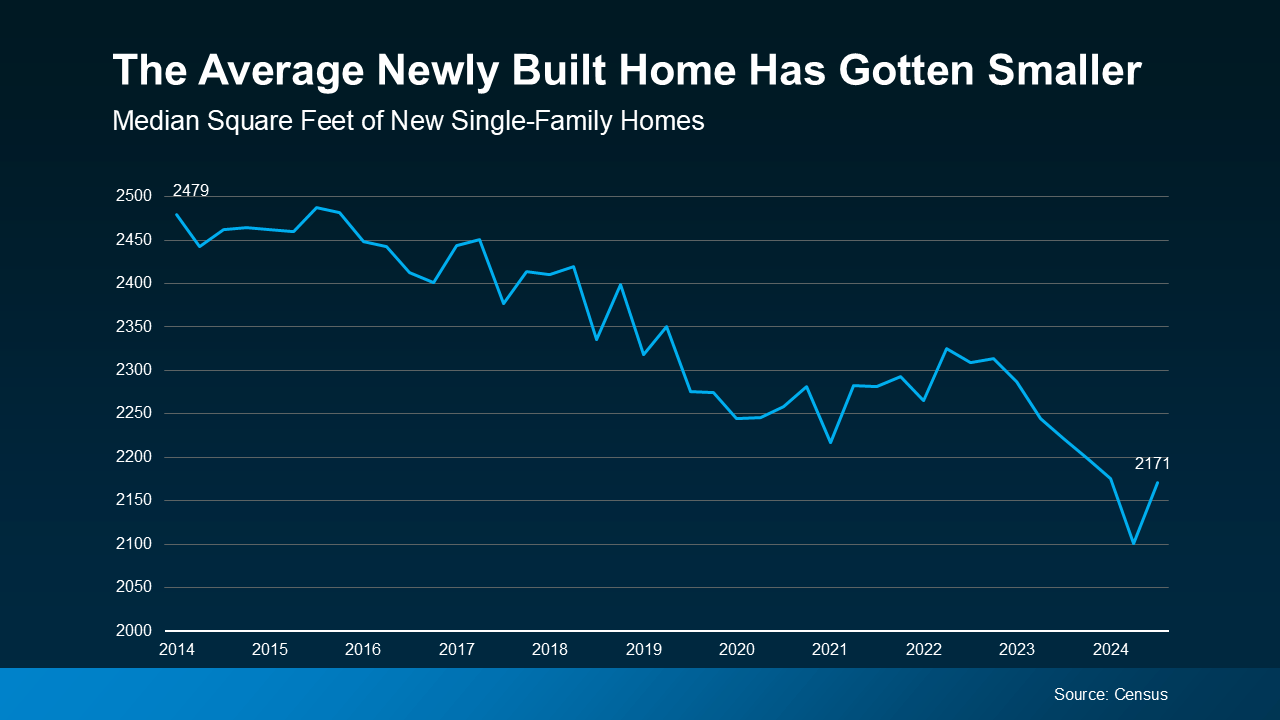

And the best part is, since builders have been focusing on smaller homes with lower price points, you may actually find out new builds are less expensive than you’d expect. So, while a lot of people write off new construction because it’s easy to assume the costs are way higher, lately, that price gap isn’t as big as you’d think. As CNET says:

And the best part is, since builders have been focusing on smaller homes with lower price points, you may actually find out new builds are less expensive than you’d expect. So, while a lot of people write off new construction because it’s easy to assume the costs are way higher, lately, that price gap isn’t as big as you’d think. As CNET says:

“If you live in an area where there’s a lot of new construction happening . . . you might be able to purchase a new house for a price similar to or even less than a pre-owned one.”

If you haven’t been able to find a home that’s in your budget, it’s time to ask your agent about new builds. If you don’t, you may have been cutting your pool of options by about a third.

Bottom Line

More choices could be the key to unlocking your homebuying goals in 2025. Reach out if you want to see what’s available in and around our area.

What features are you looking for in your next home? Let me know and I’ll put together a list of homes you’d love.

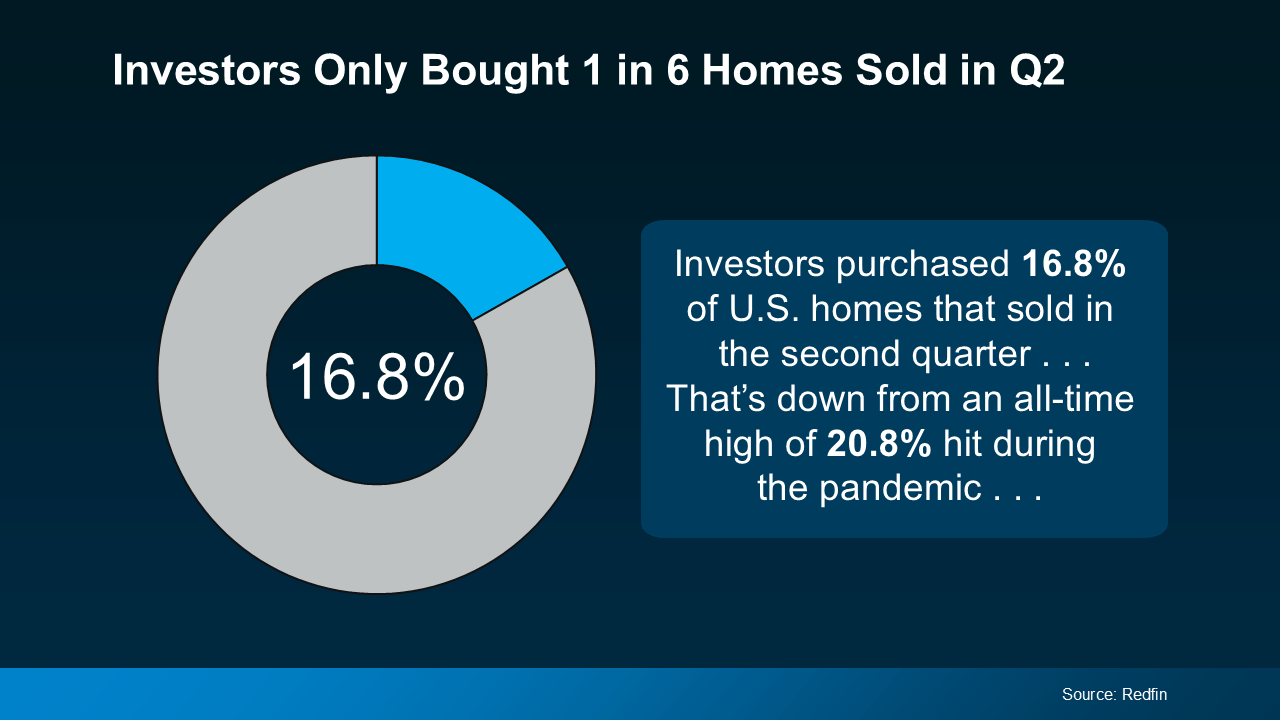

Here’s what that means. Five out of every six homes are being purchased by everyday

Here’s what that means. Five out of every six homes are being purchased by everyday